Finding the right bank to open a checking/savings account with can feel inconsequential, but one thing that may not be readily apparent is that your checking/savings account is a product just like your latest iphone. Banks compete with each other to attract and store your money in a few (simplified ways):

- Customer Acquisition: Through sign up rewards and marketing

- Ease of Use: Accessibility of physical locations and ease of use of user interfaces online features like money transfers or bill pay

- Customer Value Proposition: Loans and Annual Percentage Yield (APY)

When evaluating banks, it is highly important to consider their products over at least these dimensions. Signup promotions, higher APY’s, easy to access virtual and physical locations can save you hundreds of dollars and a meaningful amount of time. One of the best places to evaluate your options is Nerdwallet, which regularly updates, organizes, and compares a large variety of consumer checking and saving account options.

While everyone should have a checking/savings account for the reasons described here and should be carefully considered for the reasons described above, there is a fundamental misrepresentation of what banks are actually offering.

Putting your money into a bank is not saving you anything.

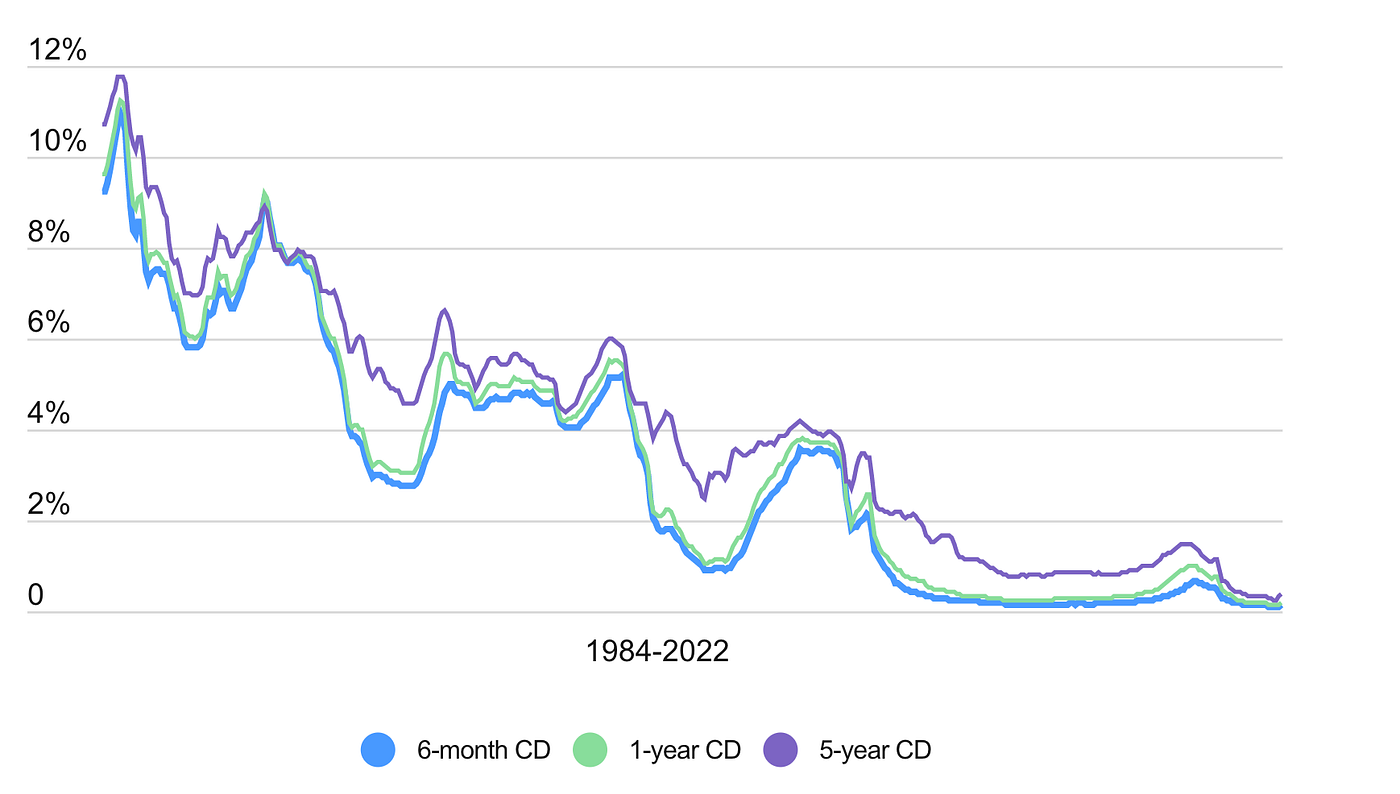

First of all, banks don’t pay you anything to keep your money in a checking account. However, if you place your money in a savings account they do. The rate that they pay you is nationally established and can be aggregated as an Annual Percentage Yield (the amount of money in percentage terms that the bank pays in exchange for holding your funds per year). Over the last 40 years this APY has fallen considerably and in line with the following Certificate of Deposit Rates (a good enough historical proxy for APY’s).

Since the peak rates in the 80’s, the return on this type of financial product has trended to rounding error away from zero. As promised, if we zero in on APY’s for the last 14 years, they a similarly low.

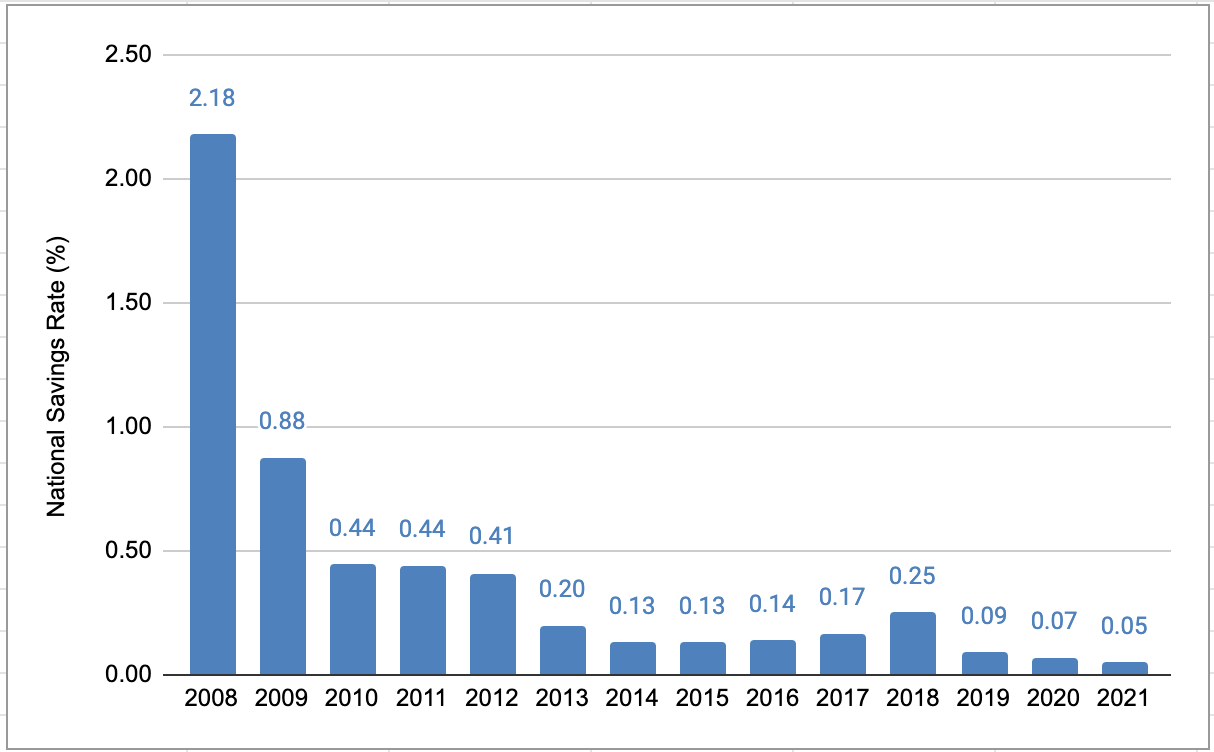

If we consider only the expected return from APY on your savings account and you had $10,000 in this account, you could expect to be paid $5 at the end of the year. At 2021 rates, all else equal, it would take you 1,387 years to double your money.

As shocking as this may seem, this is the best case scenario under current rates, there is an even more unfortunate consequence to storing money in a bank account and it’s: inflation.

For the purposes of this blog, inflation simply means that the the price of goods increase over time (if you want to learn more follow the link). It’s in part, the reason why soda was a nickel 50 years ago but is a few dollars today.

The rate at which inflation takes place, or items become more expensive, can be a real problem for individuals with a lot of money in a savings account. The issue with this capital allocation strategy is that money in the savings account only increases by the APY the bank committed to, which is extremely small today. This means that the amount of money you have in the bank largely stays the same but the cost of everything outside of your bank account is rising.

If you take your APY, the return on the dollars in the bank and subtract the percent of annualized inflation you can get a clear sense for the impact that this difference can have on your spending power.

Let’s take the previous savings rates and compare them to inflation rates over the last 14 years:

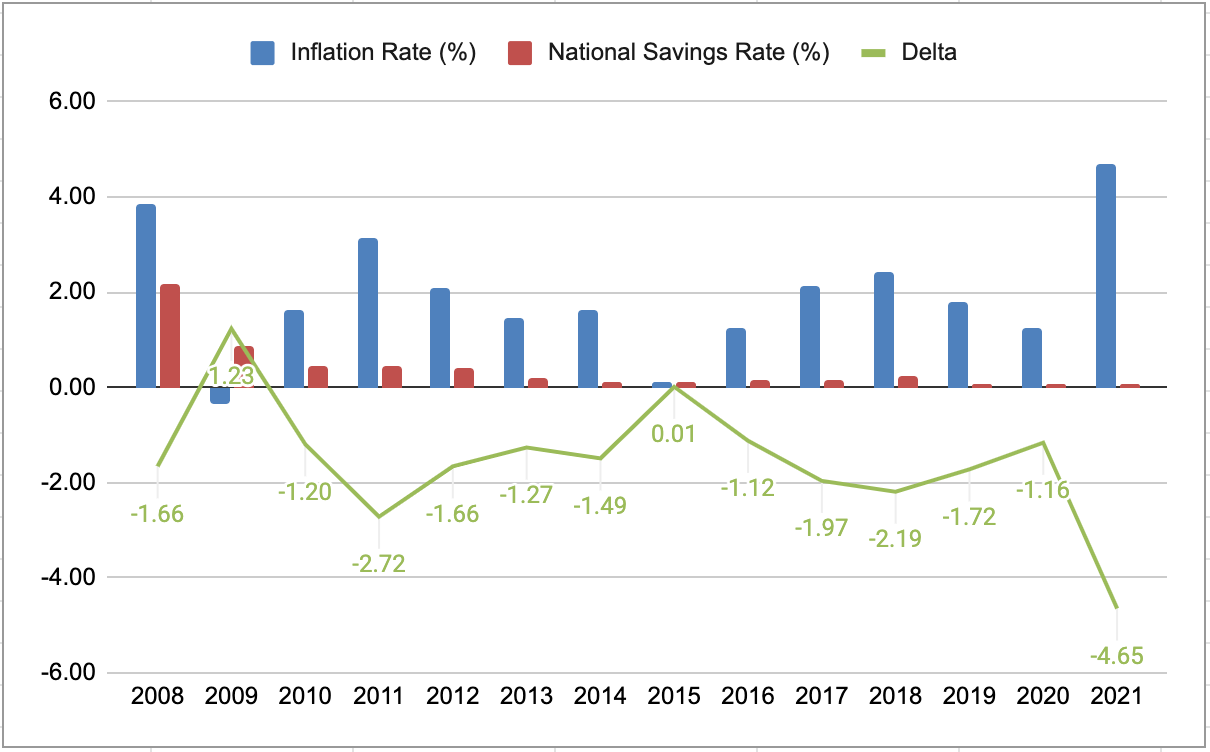

The green line represents the Gain/Loss in spending power that money in a savings account would lose each year. The greater the inflation rate and the lower APY the greater the loss in spending power. If you deposited $10,000 in savings account in 2008, you would have seen your account grow to $10,570 , however, you would have lost 22% of your spending power because your APY returns were outpaced by the rise in the cost of goods generally. Your initial $10,000, is really worth only $7,800, materially less than the initial $10,000 deposit.

Takeaway: Savings Account don’t protect your money in the way they are marketed, and in virtually all cases you will end up worse off if you are depositing large sums into a savings account. In practice, people should only be using these accounts to keep a small amount of money to cover unexpected costs and rarely expect to generate any meaningful return from their savings account. In my case, a few thousand dollars to cover an unexpectedly high credit card bill for example. Alternatively, your money needs to be put work in the form of other investment options, which we will cover in depth in a future blog.

A few final callouts…

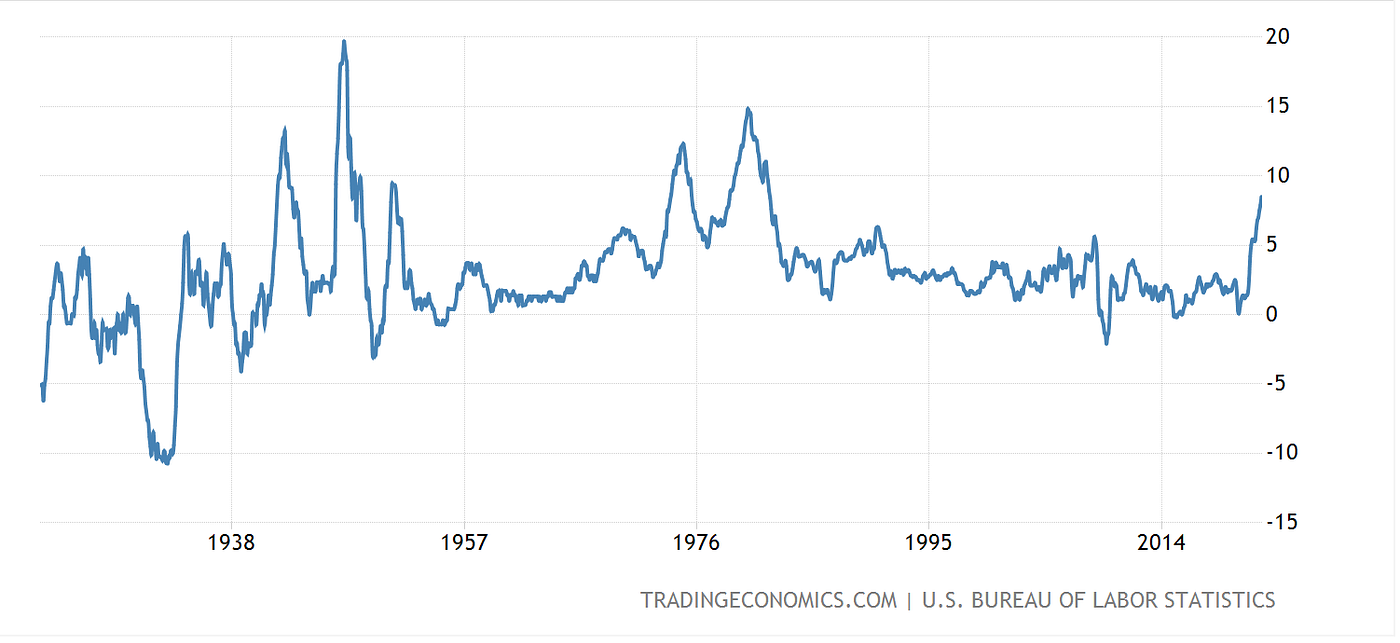

The likelihood of negative inflation: One of the only instances that your money is better off in a bank account is in the case of a deflationary environment, where prices become less expensive. The following chart that covers the last ~90 years of U.S. inflation rates likely tells you all you need to know:

Prior to 1938 is the only sustained deflationary environment and there are only a few years since then where inflation has been or approached negative rates.

The marginally better alternative, the High Yield bank account: Banks that offer accounts with particularly high APY’s are called High Yield Savings Accounts. These are online banks (no physical footprint) that pay out materially more than the products of typical large banks. For example Marcus by Goldman Sachs is paying out at 0.50% APY vs. the national APY rate of 0.1%. This effectively 5x more on an annual basis. While seemingly attractive make sure you are doing the back of the envelope math to understand the value of this switch. For example, multiply your total expected deposited amount (how much you are going to keep in the account) by the APY. (Ex. $1,000 *0.5% APY = $5). Compared to the national APY of 0.1% where you earn $1 the switch is going to improve your standing by $4. For this reason, so should never consider a bank account an investment or consider keeping a large portion of your money in one of these accounts.

Generally, I like to use these types of accounts in conjunction with a traditional large bank account to store a cash safety net. This allows me to collect for free on the higher APY while also giving me the stability and convenience (ie. ATM access, access to quarters, loans etc.) of a traditional banking operation.

All financial environments are fluid: Advice that is sound today may not be if macroeconomic conditions change materially or any number of personal circumstances warrant long or short term action.

Additional Citations

“The Fed’s Tools for Influencing the Economy.” Investopedia, 29 Aug. 2021, www.investopedia.com/articles/economics/08/monetary-policy-recession.asp.

Bessette, Chanelle. “9 Best Checking Accounts of AUGUST 2021.” NerdWallet, 30 July 2021, www.nerdwallet.com/best/banking/checking-accounts.

{kind=link}

Leave a comment

All comments are moderated before being published.

This site is protected by hCaptcha and the hCaptcha Privacy Policy and Terms of Service apply.